If we look past a few years when blockchain technology started making headlines, most people associated it with cryptocurrency. But today, blockchain technology is integrated in almost every sector in one way or another. For example, a startup can launch a decentralized finance platform. In healthcare, it can be used to secure confidential medical data on a distributed ledger. A logistics company can improve transparency by live shipment tracking.

Businesses integrating blockchain technology are seeing measurable impact, as it can decrease operational costs as low as 33 percent. The transparency and automation reduces settlements times up to 80 percent.

If you’re considering blockchain for your business, you would obviously be wondering how to create a blockchain app. You should know that blockchain app development involves complex development tasks, unlike traditional applications. Blockchain development includes smart contracts, decentralized networks, and secure architecture. These are important to increase security, automate transactions, and build user trust.

To make sure the development process excels in the right direction, working with an experienced blockchain app development services provider can make all the difference. In this guide, you will learn what a blockchain app is, how to develop a blockchain app, costs, timelines, challenges, and common mistakes to avoid.

What Is a Blockchain App?

Blockchain applications, also called decentralized apps (DApps), rely on a distributed peer-to-peer network of computers, unlike conventional apps that depend on a central server. The benefits of blockchain technology in apps are transparency, immutability, and security, allowing users to directly use it without any intermediaries. Having a clear understanding of these key elements explains why the use of blockchain technology is increasing across industries.

Smart Contracts

Smart contracts function as automated programs that execute contracts without human input by handling all aspects of contract execution. This automation of contracts enhances speed and ensures reliable performance. The contracts require distributed ledger technology to authenticate and document all operational activities. Here is what a distributed ledger is.

Distributed Ledger

Consider this as a permanent and secure memory location where all the records of transactions are saved. Every entry needs to be verified by the network, which creates a record trail that can be audited later. Having a trackable record ensures a rock-solid security and accountability. Now that you have built a foundation for blockchain applications, let’s move to the types of blockchain technology.

Types of Blockchain

- Public Blockchains: permit public access to their complete operations, common examples are Ethereum and Solana.

- Private Blockchains: Restricted access, ideal for enterprises that need control and privacy.

- Consortium Blockchains: Operate as shared resources between selected organizations that need to maintain both their operational activities and their governance practices.

The application purpose, target audience, and required security features determine the right type of blockchain selection.

Real-World Examples

Blockchain apps are already transforming industries with practical use cases:

- DeFi platforms: Enable lending, borrowing, and trading without banks.

- NFT marketplaces: Securely sell and verify digital assets.

- Crypto wallets: Give users full control over digital currencies.

- Supply chain tracking systems: Provide real-time visibility and accountability.

- Identity verification apps: Protect sensitive data while confirming authenticity.

With a combination of smart contracts, decentralized networks, and ledgers, blockchain apps provide features that are impossible for a traditional app. This basic knowledge sets the stage for you to move confidently towards the blockchain app development process. Let’s dive deep into how a blockchain app is developed from idea to launch.

Step-by-Step Guide to Develop a Blockchain App

Let’s understand this with a real-world example. Think of a fintech startup that wants to build a peer-to-peer loan lending application. The founder’s objective is faster approvals, transparent loan records, and self-executing payments without a third-party input. Although the idea looks wonderful, developing an actual secure and transparent blockchain app requires strategic technical planning. In this case, blockchain is adding real value to the businesses, but it is not the same for everyone.

So, take a moment before considering blockchain integration. Each decision you make will have a direct impact on the performance of the app. Below is the blockchain app development process discussed in detail to help you how you can create a blockchain app for your business.

1. Define the Problem and Use Case

Think twice before making that decision because not every business requires blockchain integration. If it is really solving a critical issue and adds value to your business, then you are good to go. Otherwise, it can unnecessarily increase the complexity, which directly affects the development cost and timeline.

Blockchain makes sense when your application requires:

- Trustless transactions where parties do not fully trust each other

- High transparency, such as public transaction records

- Tokenization, where digital assets or rewards are part of the model

For example, smart contracts execute automatically when the contract requirements are completed, so a Defi lending platform will benefit from it because it speeds up the operations and ensures an extra layer of security. But a simple employee management software has no benefit from blockchain technology.

So a clear purpose saves you from unwanted technical efforts.

2. Choose the Right Blockchain Type

Once you have made up your mind that blockchain technology is necessary, it’s time to select the right blockchain type. Here is what each type of blockchain brings to you:

- Public blockchains are open network blockchains that anyone can access. They benefit from publicly available apps, token ecosystems, and DeFi products. Common examples are Ethereum and Solana.

- Private blockchains are hyperledger-based systems that allow access to only authorized individuals. This is ideal for enterprise organizations that want full privacy and control. Common examples are Hyperledger and Corda.

- Consortium blockchains operate as permissioned networks that maintain semi-decentralized control through multiple organizations that manage the network instead of a single entity or public users. These are suitable for industries like banking and logistics, where multiple trusted entities are involved in governance.

You should decide on the basis of how much control you need, regulatory considerations, and the level of transparency your users need.

3. Select the Right Blockchain Platform

After deciding on the blockchain type, next you have to choose a platform. Each one has its own pros and cons. Select the one that is ideal for your business. Below are the common platform types.

- Ethereum is a popular choice among users and supports a large ecosystem of tools and developers. It supports both DeFi and NFT projects, together with advanced smart contract functionality.

- Polygon enables users to make cheaper transactions between its network without losing compatibility with Ethereum. The system delivers effective performance for applications that need to reach multiple users.

- Solana is known for a high-throughput system that enables quick transaction processing to support demanding applications.

- BNB Chain offers affordable transaction fees, which make it a preferred choice for token-based ecosystems.

- Hyperledger Fabric serves as a business solution that enables companies to create closed-access networks.

Carefully select the platform because it will have a direct impact on the development cost and timeline.

4. Design Smart Contracts

Smart contracts define how your blockchain application operates through their automated execution of rules, which handle digital assets, permissions, and operational processes.

Most public blockchain projects use Solidity (Ethereum-compatible chains) or Rust (used in Solana). The choice of language carries importance, but security stands as the primary concern.

A strong approach includes:

- Keeping contract logic simple

- Avoiding unnecessary complexity

- Conducting thorough code reviews

- Performing independent security audits

This phase requires careful attention because smart contracts are very difficult to modify once deployed.

5. Plan the Architecture

Blockchain is a part of the application. A complete software requires important components such as the frontend (user interface), backend service, and cloud-based infrastructure.

Key architectural decisions include:

- On-chain vs. off-chain logic – only essential data should be stored on-chain to decrease operational expenses.

- Backend services – handle user information together with notification systems and analytic processes outside the blockchain network.

- Node infrastructure – requires users to choose between operating their own nodes or utilizing services from infrastructure providers.

- APIs – establish a connection between your application and the blockchain network.

Balanced architecture improves performance while controlling charges and latency.

6. Develop the Frontend

Users interact with the interface, not the blockchain directly. The application will gain more users through a better user experience. The following frontend frameworks are commonly used by developers:

- React

- Next.js

- Vue

These frameworks allow users to sign transactions and interact with smart contracts. Web3 libraries facilitate frameworks to integrate with blockchain. Make sure the user interface is less technical and offers easy navigation, so every type of user can use it.

7. Integrate Wallets

Wallet integration is an important part of a blockchain app development process. Signing transactions and managing digital assets cannot be done without a wallet.

Popular options include:

- MetaMask for browser-based interactions

- WalletConnect for mobile and cross-device connections

Security is critical here. The application must not store private keys because users have complete control over their private keys. It needs clear prompts and transaction confirmations to decrease user confusion and build trustworthiness.

8. Test on a Testnet

You should deploy your smart contracts to a test network before you launch your project. This enables you to test actual transactions through a simulated environment that does not require real money. The testing process needs to include:

Testing should include:

- Unit testing for individual contract functions

- Integration testing between the frontend and the blockchain

- Security testing to identify vulnerabilities

Skipping this phase can lead to costly errors once the app is live.

9. Deploy to Mainnet

You should start deploying your contracts to the main network after finishing your testing process. This step makes your application publicly accessible.

Focus on:

- Proper smart contract deployment scripts

- Gas fee optimization to reduce transaction costs

- Monitoring tools to track performance and detect issues

After deployment, the system requires ongoing monitoring and maintenance work. The blockchain application needs complete preparation because its operations cannot depend on temporary solutions once it’s deployed.

How Long Does It Take to Develop a Blockchain App?

Blockchain app development timeline varies depending on factors like complexity, scale, and third-party integrations. As the complexity level increases, the development time prolongs as well. For example, a simple token-based MVP will take less time to develop compared to a complex enterprise blockchain solution. Here are the blockchain app development timeline estimates according to app categories.

1. Simple MVP (3–4 Months)

A basic blockchain app with limited features, such as token transfers, wallet integration, and a clean frontend, can typically be built within three to four months. The project requires smart contract development, frontend integration, and testnet testing before mainnet deployment. The purpose of MVPs is to test essential business concepts instead of delivering complete product solutions.

2. Mid-Level Application (4–8 Months)

Your app development schedule will need more time when your application includes advanced smart contract functions, multiple user roles, analytics dashboards, and third-party integrations. Security reviews, together with advanced testing procedures, will require additional time. Most mid-level blockchain applications fall within the four to eight-month range.

3. Enterprise-Grade Solution (9–12+ Months)

Enterprise blockchain platforms usually require private or consortium networks together with strict compliance standards and complicated system architecture. The projects need architectural design work together with multiple audits and comprehensive testing of system performance. The project timelines will take more than one year to complete because of both regulatory requirements and operational needs.

Typical Development Timelines for Common Blockchain Applications

| Blockchain App Type | Estimated Timeline | Key Development Components |

| DeFi Platform | 5–8 months | Complex smart contracts, lending/borrowing logic, dashboards, wallet integration, extensive testing |

| NFT Marketplace | 4–6 months | Minting and trading features, wallet integration, user profiles, analytics, frontend UI |

| Crypto Wallet | 3–5 months | Multi-currency support, secure key management, transaction tracking, and wallet connectivity |

| Supply Chain Tracking System | 5–9 months | Product tracking, IoT/ERP integrations, smart contracts, dashboards, security testing |

| Identity Verification App | 4–7 months | Secure digital ID storage, authentication, privacy compliance, smart contracts, frontend integration |

What Impacts the Timeline?

Several factors influence how long development takes:

- Smart contract complexity – More logic means more testing and review.

- Security audits – Essential but time-intensive.

- Regulatory compliance – Especially in finance or healthcare sectors.

- Team size and expertise – Experienced blockchain developers can reduce delays.

- Feature set and integrations – The broader the scope, the longer the build.

Perhaps the feasibility study is the next logical milestone that really helps in making the project successful.

How Much Does Blockchain App Development Cost?

Blockchain app development cost is not the same for every project. It is influenced by constraints like complexity, scale, infrastructure, and intended outcomes. That means a lightweight MVP could cost less than an enterprise platform that has to handle a huge volume of transactions. Here are the estimated cost types according to app category.

1. MVP: $25,000 – $60,000

A minimum viable product (MVP) usually comes with basic smart contracts, wallet integrations, and a minimalist user interface. The objective of an MVP is functionality, early user feedback, and enhancements according to that. Primary cost factors in this phase are core development, initial testing, and testnet deployment. It is an ideal option for startups to test market demands.

2. Medium Complexity: $60,000 – $120,000

Medium complexity apps are those with advanced smart contracts, multi-user roles, dashboards, and third-party integrations. So, as the features increase, it requires more development time and testing as well. Deeper testing, backend services, and security reviews have to be done more rigorously at this stage, which eventually increases the overall development cost.

3. Enterprise Solution: $150,000+

Enterprise blockchain platforms need complex infrastructure, compliance planning, private or consortium networks, and multiple audits. This category of blockchain platforms includes a detailed architecture design and continuous technical support, which significantly increases the cost.

Estimated Costs for Common Types of Blockchain Applications

| Blockchain App Type | Estimated Development Cost | Typical Features Included |

| DeFi Platform | $80,000 – $150,000 | Lending/borrowing protocols, smart contracts, token integration, and user dashboards |

| NFT Marketplace | $60,000 – $120,000 | Minting/selling NFTs, wallet integration, user profiles, and marketplace analytics |

| Crypto Wallet | $50,000 – $100,000 | Multi-currency support, secure key management, transaction tracking, and wallet connectivity |

| Supply Chain Tracking System | $70,000 – $140,000 | Product tracking, smart contracts, dashboards, integration with ERP or IoT devices |

| Identity Verification App | $60,000 – $130,000 | Secure user authentication, digital ID storage, compliance with privacy regulations, and smart contracts |

What Influences the Blockchain App Development Cost?

Several factors shape the final investment:

- Blockchain platform choice – Development on Ethereum and other networks requires extensive work to achieve optimal gas usage. The Hyperledger framework needs custom-built systems for its development process.

- Security audits – Independent code audits establish essential requirements that result in increased operational expenses.

- UI/UX design – Designers must dedicate their efforts to creating interfaces that achieve both clarity and user-friendly design.

- Third-party integrations – APIs, payment gateways, identity services, or analytics tools increase development time.

- Ongoing maintenance – Smart contract monitoring, upgrades, hosting, and security updates add recurring expenses.

These are estimated price ranges to help you decide which category your blockchain app development idea falls in and how much it will cost.

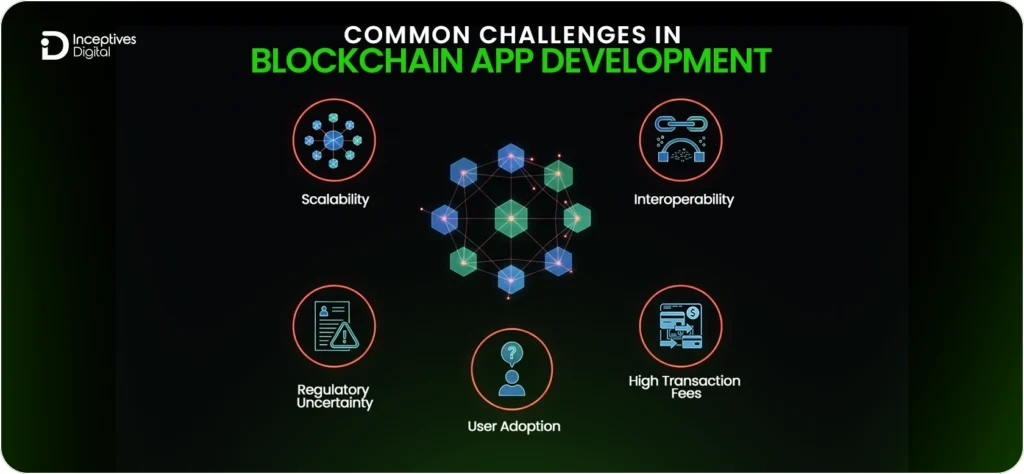

Common Challenges in Blockchain App Development

Blockchain app development process comes with its own unique challenges, unlike traditional applications. Early identification of these issues proves helpful in avoiding unwanted delays and costly reworks.

1. Scalability

Blockchain networks can face difficulties when they need to process large numbers of transactions. Lack of proper system design and optimization methods will cause applications to function at reduced speeds, which will result in user dissatisfaction and business limitations.

2. Interoperability

Different blockchains use different protocols, which create challenges for applications wanting to operate between different networks. Creating seamless platform integration with existing systems requires both strategic design work and extra programming resources.

3. Regulatory Uncertainty

Different countries have different blockchain regulations that frequently change with time. Regulations for financial data privacy and digital asset laws create a complex compliance situation that leads to penalties and restricted access for those who fail to meet requirements.

4. High Transaction Fees

Blockchain systems experience changing gas fees, which create high expenses for users who need to conduct multiple transactions. The smart contract optimization process, together with the assessment of layer-2 solutions, helps to decrease operational expenses.

5. User Adoption Barriers

Blockchain applications can feel overwhelmingly technical for new users. Poor user experience, unclear transaction process, and confusing wallets can heavily impact user attraction and retention. Educating the users and providing an easy user interface increases engagement and user retention.

By tackling these challenges strategically through smart architecture, guidance, cost optimization, and a smooth user interface, businesses can successfully design and develop a blockchain application that fosters real business growth.

Common Mistakes to Avoid in Developing a Blockchain

Even the most promising blockchain projects can stumble if key mistakes are overlooked. Businesses that understand common pitfalls that lead to application failures can save time and reduce costs while creating secure applications that users can easily use. Here are the common mistakes you should avoid in your blockchain app development process.

1. Using Blockchain Without a Real Need

Carefully evaluate whether decentralization adds value to your project or not. If there is no need to integrate blockchain, then don’t do that. It will only increase the complexity, cost, and development time without delivering enough return on investment.

2. Ignoring Security Audits

Smart contracts become permanent after their deployment. Security audits need to be completed because skipping them creates security weaknesses, which result in financial losses and damage to the organization’s reputation.

3. Poor Tokenomics Design

The platform experience will suffer from user decline because the token model loses its effectiveness to keep users engaged and the platform operational.

4. Weak User Experience (UX)

Technically sound apps will fail when users experience confusion during their use. A complicated interface can reduce adoption and trust.

5. Underestimating Gas Fees

Public networks often have fluctuating transaction costs. Ignoring this can frustrate users and impact app viability.

Public networks experience changing transaction costs. The failure to recognize this issue creates user frustration, which leads to negative effects on application performance.

6. Not Planning for Scalability

Blockchain applications need to manage growth with their existing capacity. The system will experience performance issues because of user traffic if it lacks a scalable architecture.

To avoid these mistakes, you need careful planning, security, and attention to user experience. Partnering with a mobile app development company having proven experience in blockchain integration is recommended to make sure your blockchain app development project stays on track.

Tips from an Experienced Blockchain App Development Company

To ensure a smooth blockchain app development process, careful planning, practical experience, and focusing on both technical and user-focused details are important. Following these tips could really help you develop a blockchain application that is secure and scalable.

Key Tips:

- Start with an MVP: Validate your idea and core features before scaling.

- Prioritize Security: Conduct smart contract audits, follow best practices, and monitor the network continuously.

- Focus on User Onboarding: Simplify wallet connections and provide clear instructions to enhance adoption.

- Plan Governance Early: Define permissions, updates, and upgrade processes before launch.

- Keep Smart Contracts Simple: Modular and concise contracts reduce errors, deployment risks, and gas fees.

- Think Long-Term Scalability: Design infrastructure and integrations to handle increasing users and transactions efficiently.

The Road Ahead for Blockchain App Development

Developing a blockchain app requires deliberate planning, a defined use case, and the right technical decision-making. Security should always be your primary focus throughout the blockchain app development process. As we know, the development costs and timelines differ depending upon various factors, as we discussed above, setting realistic time and budget expectations is critical. If you approach it with the right strategy, it is very obvious that your blockchain application will deliver transparency, security, and long-term value.

If you are looking for blockchain app development services, choose the one that has a proven portfolio in blockchain app development and understands the architecture, security, compliance, and user onboarding as well. The right guidance could help launch your project with confidence, which cultivates real business outcomes.

CTA SECTION START

cta title: Create a Blockchain App That Solves Real Business Problems

cta des: Turn your idea into a secure, scalable blockchain app that boosts efficiency, transparency, and growth for your business.

cta button: Get Started Today

CTA SECTION END

Blockchain App Development FAQs

No. Blockchain is useful when you need decentralization, transparency, trustless transactions, or tokenization. If a traditional database can solve the problem efficiently, adding blockchain may only increase complexity and cost.

Blockchain apps can be highly secure when developed properly. However, security depends on smart contract quality, audits, key management, and infrastructure setup. Poorly written contracts or skipped audits can create serious vulnerabilities.

Smart contracts are generally immutable once deployed. Updates are possible through upgradeable contract patterns or governance mechanisms, but these must be planned during the architecture stage.

Scalability depends on network limitations, smart contract efficiency, infrastructure design, and user load. Solutions such as layer-2 scaling, optimized code, and hybrid on-chain/off-chain architecture can improve performance as usage grows.

SIDEBAR LIST START

- How to Create a Blockchain App?

- What Is a Blockchain App?

- Step-by-Step Guide to Develop a Blockchain App

- How Long Does It Take to Develop a Blockchain App?

- How Much Does Blockchain App Development Cost?

- Common Challenges in Blockchain App Development

- Common Mistakes to Avoid in Developing a Blockchain

- Tips from an Experienced Blockchain App Development Company

- The Road Ahead for Blockchain App Development

- Blockchain App Development FAQs

SIDEBAR LIST END